En

EnThe third quarter of 2018 brought a tumult of completed and newly started trade deals for the administration of President Donald Trump. Six ongoing deals will define the success of the President’s trade policy approach ahead of the midterm elections, and beyond.

The renegotiated NAFTA deal, reborn as the U.S.-Mexico-Canada Agreement (USMCA) has been agreed in principle but has yet to be signed. The biggest risk is whether an obstructionist Congress post-elections agrees to sign it or not.

The punch and counter-punch of tariffs against Chinese exports, started by the section 301 review of intellectual property rights, has no clear “off-ramp” at this stage. The next move is for President Trump to decide whether to escalate duties to cover all of China’s exports and run the risk of further retaliation.

New trade negotiations have been started with both the European Union – which will likely focus on technical barriers to trade rather than tariffs – and Japan. The latter will likely take the longest to achieve given the requirements for Congressional consultations.

In the meantime negotiations with India are less formal and still ongoing, though tackling what the President has called “The Tariff King” will require balancing the needs of Make-in-India with Make-America-Great-Again.

Finally the Taiwanese government has called explicitly for free trade negotiations. That’s exactly what the Trump administration is looking for, but would lead it into a geopolitical quagmire.

(1) USMCA – Updated NAFTA Needs to Clear Congress

NAFTA is reborn as USMCA following the conclusion of negotiations between Canada and the U.S. to join the prior deal struck between Mexico and the U.S. The revised text will now be reviewed by each country’s parliaments in order to allow the deal to be formally signed by November 30. The major sticking points relating to dairy and dispute settlement were resolved, though from an economic – and Trump administration policy – perspective it was a solution to rules of origin that mattered most. The automotive sector, where U.S. imports totaled $138 billion in the past 12 months, has been the main focus.

The near-term impact on auto supply chains should be minimal given (a) most standards are phased in through 2023 and beyond and (b) the caps on parts exported to the U.S. from Canada and Mexico are 2.7x their current levels. Additionally there are limits on passenger vehicle exports that are 54% and 43% above current levels from Canada and Mexico to the U.S. Those ceilings equate to 54% of current total U.S. imports and may present a future challenge to striking trade deals with Japan and the EU. They too in total accounted for 54% of U.S. vehicle exports in the past year.

Read more → (First published Oct. 1)

Source: Panjiva

(2) China Tariffs – $250 billion Off-Ramp or $270 billion Escalation?

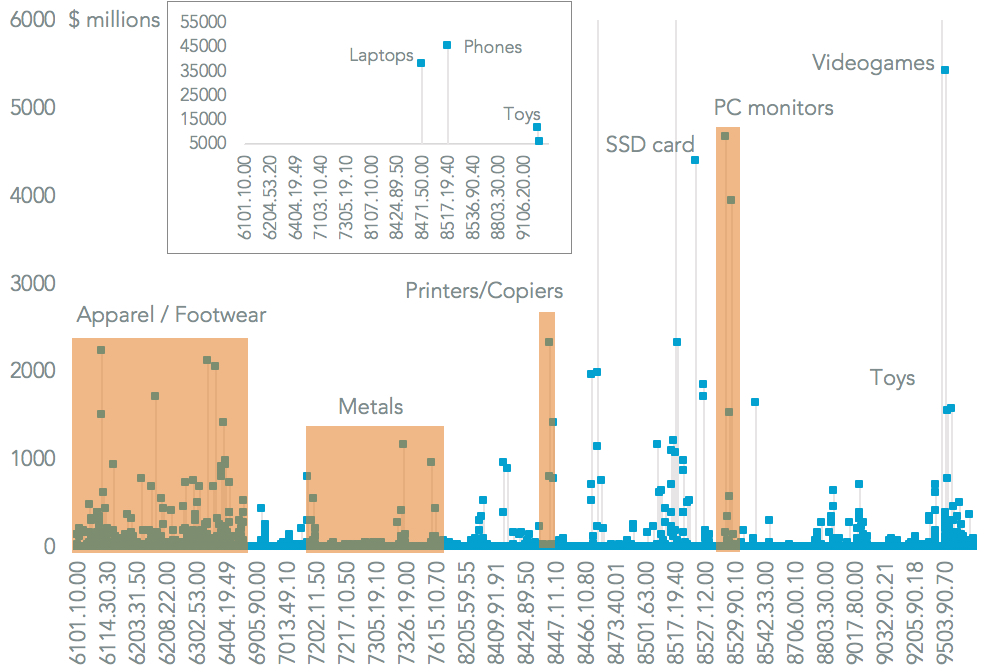

The Chinese government’s decision to not engage in talks with the U.S. after the bilateral imposition of duties on $360 billion of trade makes it more likely President Trump will go ahead with his threat to apply duties on all Chinese exports. There were 8,656 tariff lines with imports worth $270 billion in the 12 months to July 31 that were not hit by the first three lists (July 6, August 23 and September 24).

There are several implementation challenges for the President. First is that several tariff lines have already been granted exemptions in previous assessments. That would rule out 128 of 1,080 chemicals products as an examples.

Secondly most remaining products are consumer goods where price increases may prove unpopular including $46 billion of mobile phones and $38 billion of laptops PCs. Targeting apparel ($27 billion) and footwear ($14 billion) for tariffs (a form of tax) is also regressive from an income perspective.

Furthermore targeting kids products ($12 billion of toys) seems politically untenable ahead of the holidays. A more nuanced approach targeting commercial products (computer monitors and printers) or those already subject to other tariffs (e.g. metals) may be more successful.

Read more → (Sept.24)

Source: Panjiva

(3) EU / U.S Trade Negotiations – Early Harvest, Tough Grains

The USTR and European Commission have said out a process to cut technical barriers to trade (TBT) that will run through late November. That should maintain momentum after the initial kick-off between President Trump and President Juncker led to a standstill in new duties. It’s unlikely though that a wider trade deal with complete tariff cuts will be delivered in the mold of TTIP. While the U.S. is applying for TPA deal approval from Congress that will likely only come after the midterms, possibly under a new Congressional makeup.

The EC may not get approval from Italy and France for negotiating authority. The $163 billion American merchandise deficit with Europe, including a record high in July 2018, will keep the Trump administration’s eye on progress and could be partly satisfied by a small selection of reduced tariffs. Longer-term tariff reductions worth $12.4 billion may be possible ($7.2 billion on EU exports and $5.2 billion on U.S. exports). Leading products for discussion should include passenger and commercial vehicles ($2.4 billion of bilateral duties), beverages ($388 million) and refined oil products ($1.0 billion) based on average MFN duties applied at the HS-4 level.

Read more → (Sept.11)

Source: Panjiva

(4) Japan / U.S. Negotiations – Hurry Up, Ask Permission, Then Wait

Negotiations to create a new Japan-U.S. trade agreement could be the defining policy action for both countries in 2019. The project, launched by Prime Minister Abe and President Trump, can’t start until 90 days after Congress have been informed of the plan. That needs to include detailed negotiating positions 30 days before the talks start.

The initial negotiations will focus on reducing tariffs. On the basis of WTO duties, Americans paid $2.9 billion of tariffs on Japanese exports while $1.2 billion was paid by Japanese buyers of American products in the 12 months to July 31. That equates to average tariff rates of just 2% in each direction. There’s plenty of potential opportunities but they may not be significant at the macroeconomic level.

The largest potential area cut U.S. import duties is in cars. The U.S. has a 2.5% rate and Japan 0% resulting in $1 billion of duties that could be cut. On the Japanese side the most significant tariffs are on beef with $655 million due to a 39% rate. There is also an opportunity to cut U.S. duties on Japanese capital goods exports. That could offset the increased costs for American industry resulting from section 301 duties on Chinese exports.

Read more → (Sept.27)

Source: Panjiva

(5) India / U.S. Negotiations – “Make America Great Again” Meets “Make in India”

The Indian government believes trade talks with the U.S. will take target of facilitation measures rather than a full trade deal. That follows President Trump’s assertion that India is ready to launch FTA negotiations. With a $22.6 billion Indian trade surplus in the 12 months to July 31 – despite a 21% surge in American exports to India – engagement with the U.S. may prove wise given the administration’s stance on deficits.

India’s imports in 2Q have been led by aerospace, coal and petrochemicals – the U.S. will want to promote oil and gas purchases too as India reduces its reliance on Iran. India’s appetite for energy can be seen in its surging imports of all products which rose by 28% in August and by 18% in the past 12 months.

Read more → (Sept.13)

(6) Taiwan / U.S. Negotiations – Where Policy Meets Geopolitics

Taiwan’s Foreign Minister has called on the U.S. to start bilateral, free trade negotiations. While that would fit with Trump administration policy both on trade and towards Taiwan there appear to have been few significant moves since a March directive from the President. That may be linked to ongoing, fractious negotiations with China. The U.S. accounted for 12% of Taiwan’s exports in the 12 months to August 31 after an 8% expansion in the past year.

Yet, Taiwan’s trade surplus of $17 billion vs. the U.S. will win it few friends in the Trump administration. Easy wins from a merchandise-led deal may prove hard to find. Taiwan is already a major importer of the American government’s priority products including high tech semiconductor making gear was 8% of imports from America in the 12 months to July 31), aircraft, oil and soybeans. There may be some room for expansion of exports of autos (1.6% of Taiwan’s imports from America, or half the proportion for all countries outside NAFTA) and pharmaceuticals (0.5%, or one third the proportion).

Read more → (Sept.14)

Source: Panjiva