En

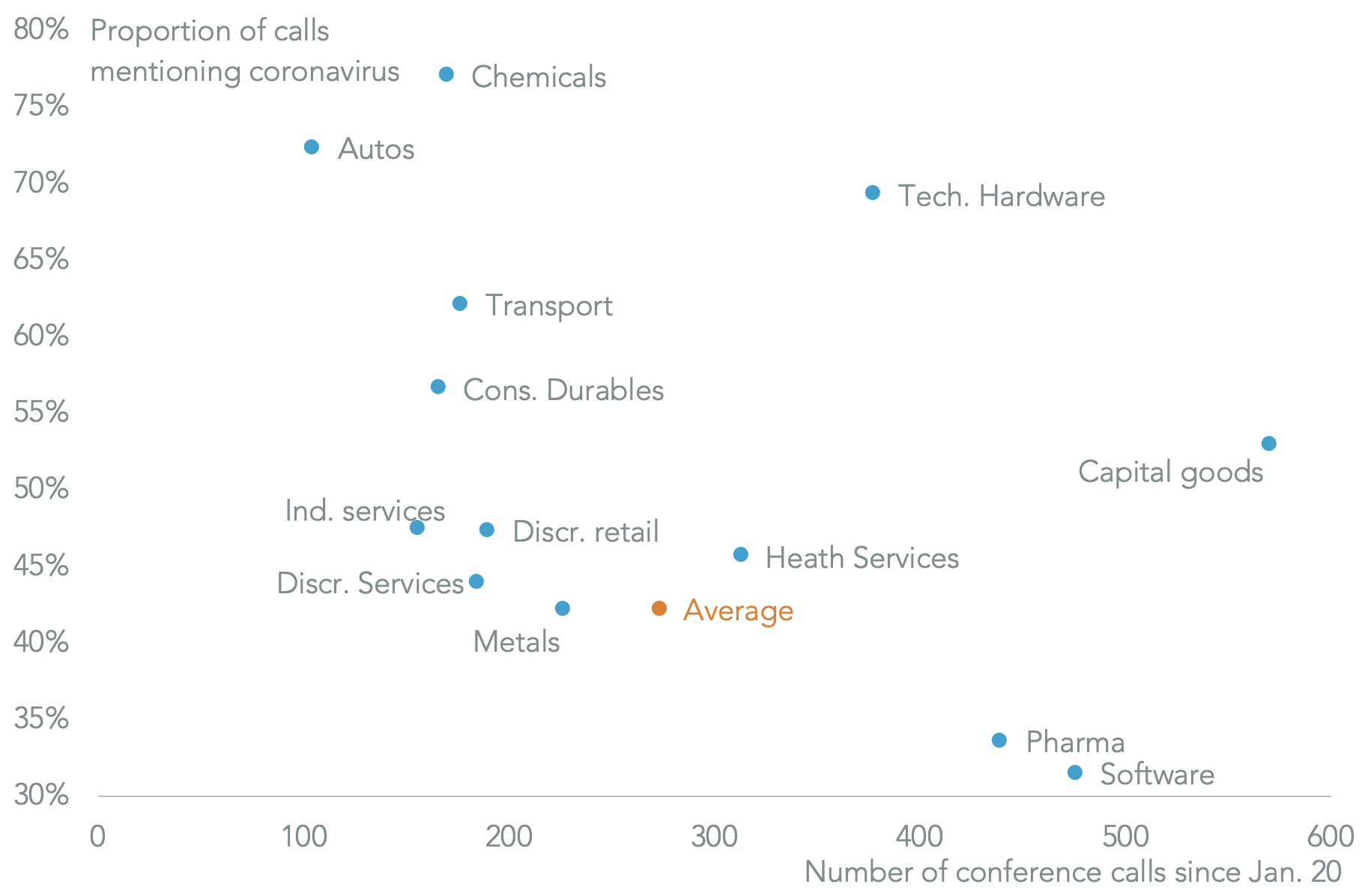

EnPanjiva’s analysis of over 6,000 conference calls since Jan. 20 via S&P Global Market Intelligence showed that 42.3% of calls discussed COVID-19 coronavirus either in management comments or investor questions. Perhaps unsurprisingly the highest rate of mentions were in the physical goods space where firms are potentially exposed both in terms of lost sales or disrupted supply chains. At a GICS-1 level the materials industry had the highest level of mentions at 57.1% of calls while utilities were just 17.1%.

Source: Panjiva

Stepping down a level of granularity the highest proportion of mentions was in the chemicals subsector of materials with a 77.1% rate of mentions. That was followed by the autos segment of consumer discretionary at 72.4% and technology hardware at 69.3%. The latter two are not a surprise given our prior analysis of supply chains in China discussed in Panjiva’s research of Jan. 28.

There was also an unsurprisingly high level of mentions in the transportation services sector which includes logistics and airlines at 62.1%. Consumer durables and capital goods manufacturing reached 56.6% and 52.9% respectively – there’s been plenty of evidence in both of disruptions to upstream supply chains.

There was a low level of mentions in the healthcare sector generally at 38.6% including just 33.6% for pharmaceuticals – potentially as few companies are actually developing coronavirus drugs and may be unaffected by active ingredient shortages so far.

Source: Panjiva

Coming back to the chemicals sector there may have been a high level of mentions due to the product-specific nature of many companies, meaning they have a high level of exposure to hard-to-find products in their upstream supply chains as well as industrial customers downstream.

One example has been tile coatings maker Ferro Corp. whose CEO, Peter Thomas, has stated “uncertainties accompanying the outbreak of the coronavirus, including its potential impact on manufacturing, supply chains and consumer sentiment“. That’s led the company to include a precautionary “headwind of approximately $1 million to $2 million to gross profit” in its Q1 figures according to CFO Benjamin Schlater. That compares to consensus pre-tax profits of $15 million for Q1 and $88 million for 2020 according to S&P Global Market Intelligence data.

Panjiva data for U.S. seaborne imports linked to the firm shows there may be signs of stockpiling with shipments up by 40.6% year over year in the first two months of 2020, compared to a growth of 9.6% in Q4.

That’s largely been down to a 90% surge in shipments from Europe while imports from China slumped by 41.7%. The latter is likely part due to drag from tariffs as much as COVID-19 linked shortages.

Source: Panjiva